A year ago, I wrote a post called, “how to time the market like Warren Buffett,” in which I proposed a very simple market timing method inspired by this passage from the Oracle of Omaha's 1992 letter to shareholders:

The investment shown… to be the cheapest is the one that the investor should purchase.… Moreover, though the value equation has usually shown equities to be cheaper than bonds, that result is not inevitable: When bonds are calculated to be the more attractive investment, they should be bought.

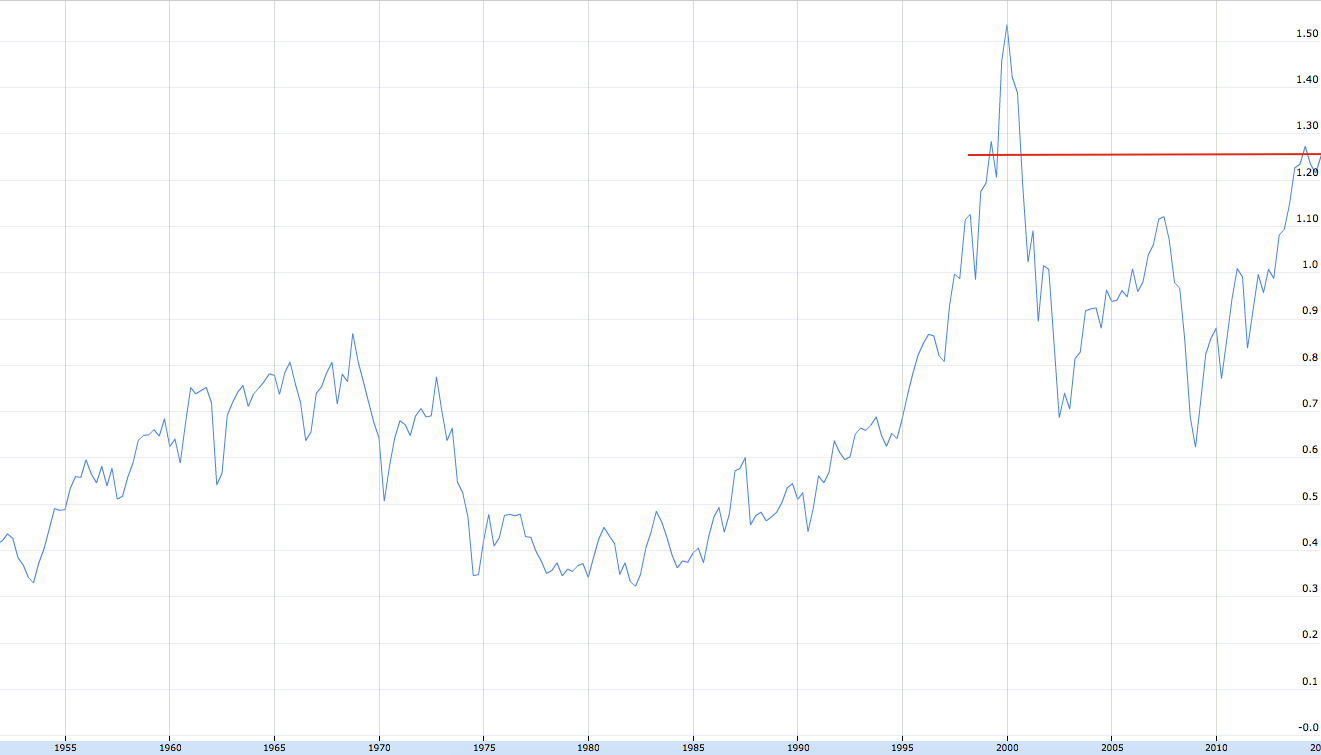

The idea is very simple and intuitive: When reliable measures forecast that stocks will outperform bonds, buy them. However, when, on rare occasion, they forecast that bonds will outperform stocks then they should be favored. But how to forecast equity returns? Simple. Just use Buffett's favorite valuation yardstick, market cap-to-GNP. Right now this measure shows stocks to be about as highly valued as they were back in November 1999.

Click on picture to enlarge

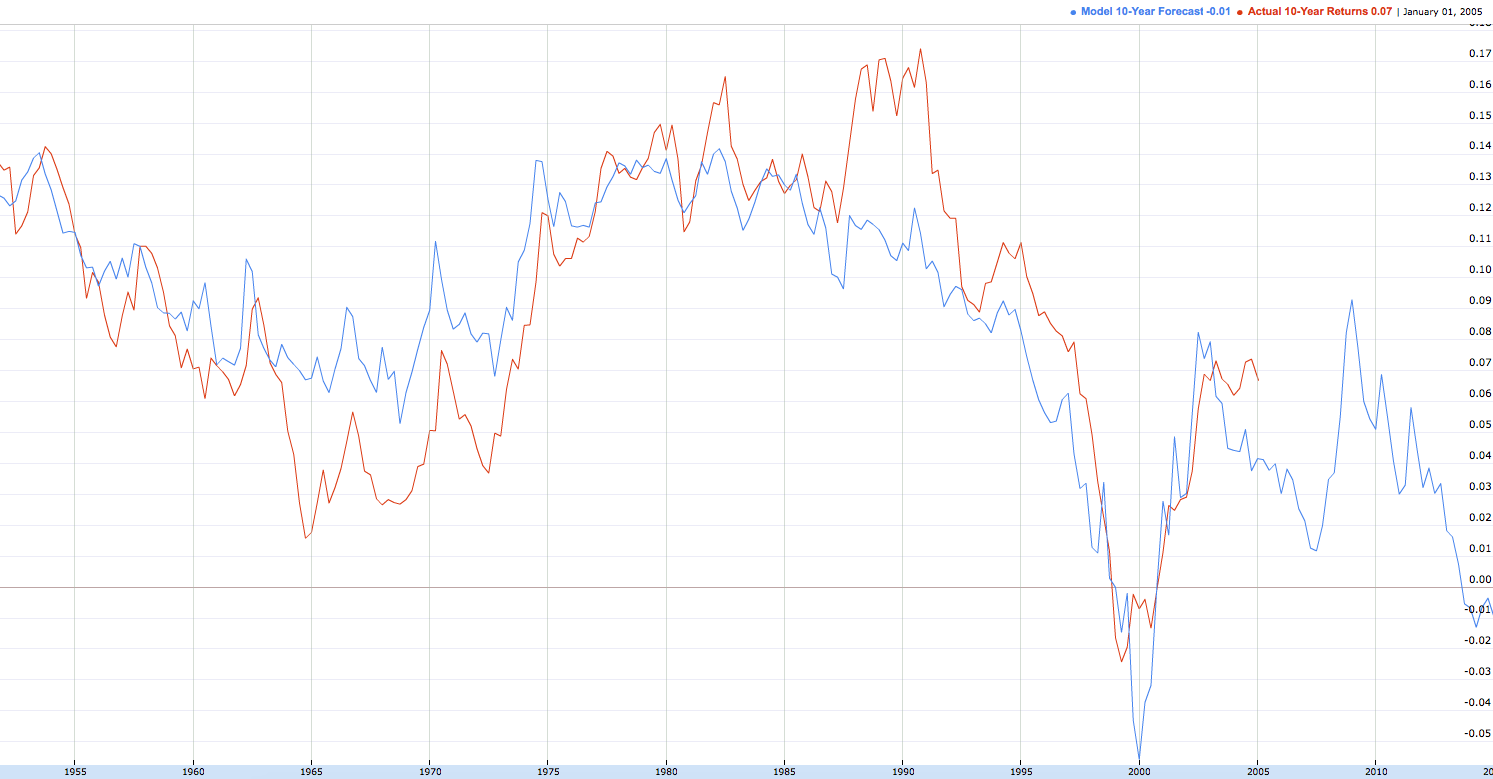

What makes this measure most valuable, though, is its forecasting accuracy – which may be what makes it Buffett's favorite. Below is the 10-year forecast implied by this measure (blue line) against the actual 10-year return for the S&P 500. Notice the red line tracks the blue fairly closely but can overshoot in both directions, overestimating returns during the 1973-74 bear market and understating returns during the dotcom bubble.

Click on picture to enlarge

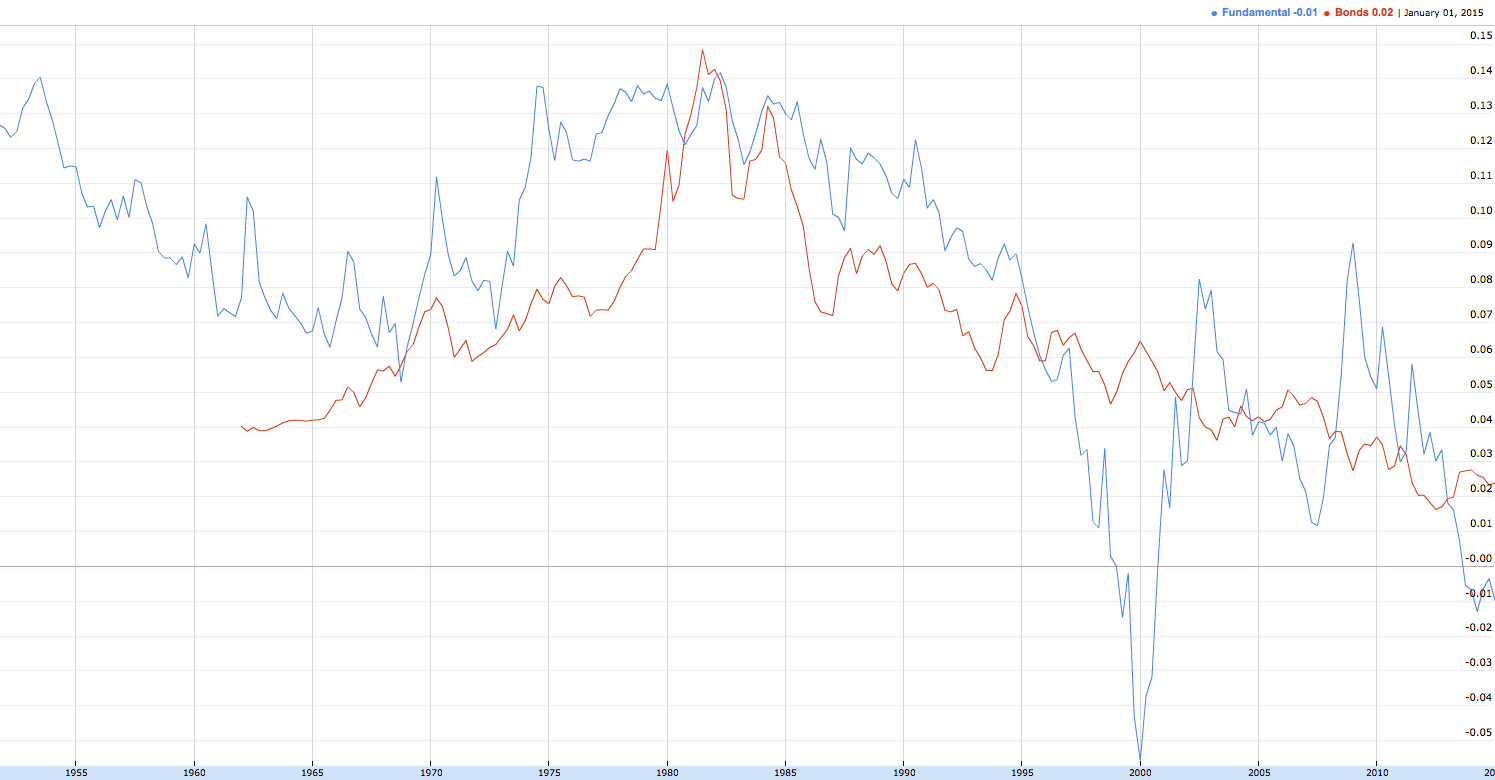

The next chart overlays the 10-year treasury bond yield (red line) against the 10-year forecast for stocks (blue line). The majority of the time this comparison suggests stocks are the better investment. There are few occasions, however, when bonds offer the better opportunity. Today is one of those occasions.

Click on picture to enlarge

In my original post, I demonstrated just how attractive it would have been to follow this methodology. Since 1962, an investor who simply had bought stocks when they were more attractive and then switched to bonds when they became more attractive outperformed a buy-and-hold approach and dramatically so (mainly by sitting out a significant portion of the last two major bear markets).