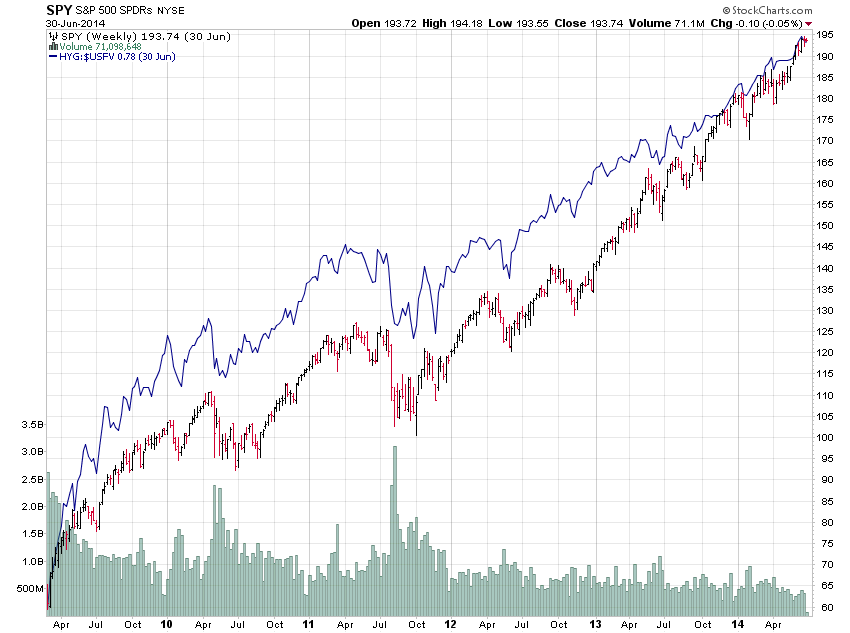

I have been watching the junk bond (and leveraged loan) market very closely over the past few months mainly because risk appetites there have been closely tied to stock prices for a very long time. In fact, since the bull market was born in March of 2009 until this summer high-yield risk appetites (as measure by the ratio of the high-yield ETF to the 5-year treasury bond) and stock prices have had a 98% correlation coefficient.

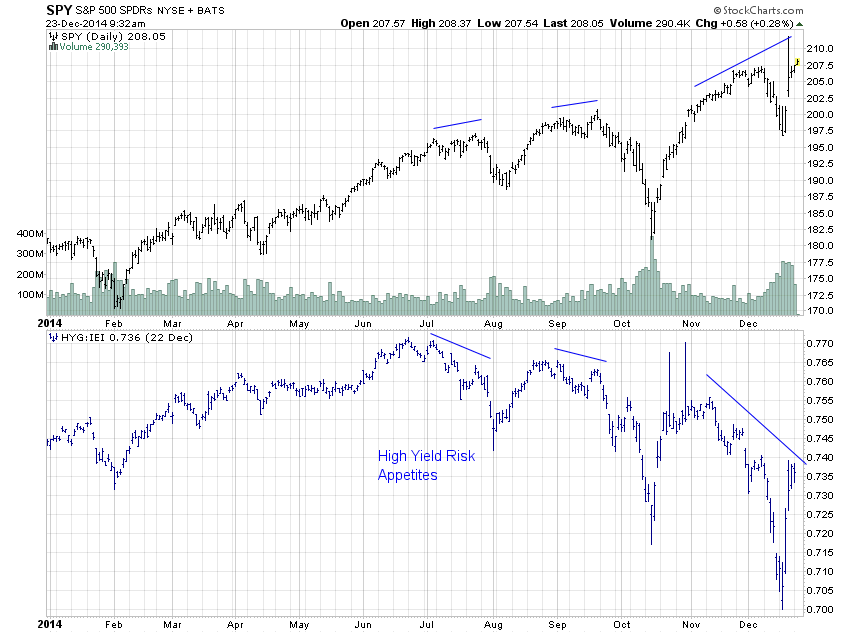

Clearly, the chart above demonstrates that the strength in junk risk appetites led stocks off the lows back in 2009. Over the past summer, however, junk bonds started to lag stocks for the first time since the bull began (or lead lower, depending on your perspective). Since then the divergence has only gotten wider with each subsequent new high in the stock market:

Clearly, the chart above demonstrates that the strength in junk risk appetites led stocks off the lows back in 2009. Over the past summer, however, junk bonds started to lag stocks for the first time since the bull began (or lead lower, depending on your perspective). Since then the divergence has only gotten wider with each subsequent new high in the stock market:

So what's going on? Why the sudden shift in equity risk appetites relative to high-yield?

So what's going on? Why the sudden shift in equity risk appetites relative to high-yield?

Well, the popular explanation has been that the junk market has a much higher exposure to energy so the oil crash will have a much larger impact. For that reason, stocks are rightly “decoupling” from the junk market, or so it goes.

To me this argument sounds more than a little specious. The energy component in junk is about 14%. This compares to an 11% weighting in the S&P 500 so there's a difference there, to be sure, but not a very significant one.

And as Howard Marks recently wrote, “It's historically unprecedented for the energy sector to witness this type of market downturn while the rest of the economy is operating normally. Like in 2002, we could see a scenario where the effects of this sector dislocation spread wider in a general ‘contagion.'”

The energy boom over the past few years, driven by fracking technology, has been a major boon to the overall economy. The fact that fracking is now unprofitable means that boom is likely to bust. Believing that the boom was a positive but the bust won't be is wishful thinking at best.