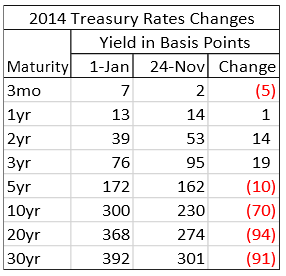

The overwhelming majority of forecasters in late 2013, believed that interest rates in 2014 would rise. They were wrong. Rates mostly went down. Two leading bond fund managers (Bill Gross and Jeff Gundlach) believed rates would remain low. They were right. Once again, most economists and primary Treasury dealers, and some Fed governors, expect that the Fed will begin raising the Fed Funds rate sometime in 2015 – that is at the very short-term end of the yield curve. While central banks are lowering their short-term benchmark rates in countries such as China and Japan, and suggesting they may do so in Europe, the generally expected direction of short-term rates in the US is up.

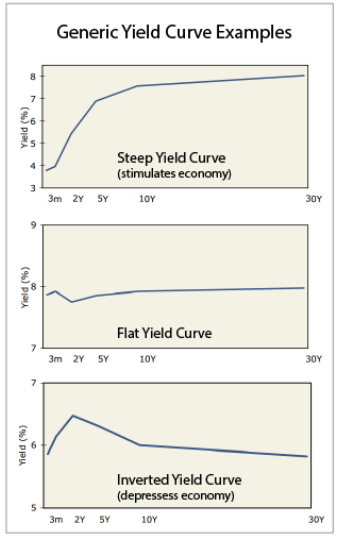

However, with US Fed Funds rate near zero, an expected rise is far from expecting punishing rates. Both Bill Gross (formerly of PIMCO and currently of Janus) and Jeff Gundlach (of DoubleLine) each expect interest rates at most maturities to remain below historic normal levels. Gross says “lower for longer.” More important that the level of interest rates, is the shape of the yield curve. A normal curve sloping up from left to right (short-term to long-term) is stimulative of lending and the economy. An inverted curve (sloping down from left to right) puts the breaks on lending and the economy.

Today, Gundlach said in an interview that “the yield curve will flatten at a low level previously thought unthinkable.” He not only sees rates low for an extended period, but actually lower than they are now.

One of Gundlach's key arguments is that with a strong US dollar and other key nations with lower Treasury rates, our current rates will continue to attract foreign investors, preventing the intermediate and long end of the curve from rising. In fact he expects them to decline.

Remember the Fed can only directly control the extreme short end it lends to banks. The market decides the other rates. Let's think about the Gundlach scenario.